Clarifies that earned wage advances are loans and that expedite fees and most “tips” are finance charges

WASHINGTON – Advocates applauded the proposed interpretative rule released today by the Consumer Financial Protection Bureau (CFPB) to address evasions by fintech payday lenders that hide the cost of 300% annual percentage rate (APR) loans and evade state rate caps. The CFPB rescinded an advisory opinion that was issued under former Director Kathy Kraninger and proposed to make clear that paycheck advances are loans that must comply with the Truth in Lending Act (TILA) and that most so-called “tips” and other junk fees are finance charges under TILA.

“A payday advance that is repaid on payday is a payday loan, and fintech cash advance apps that call themselves ‘earned wage access’ are just high-cost lending in disguise,” said Lauren Saunders, associate director of the National Consumer Law Center. “The CFPB has seen through fintech payday lenders’ new clothes, making clear that worker payday loans that hide 300% APRs in coerced, so-called ‘tips’ and other junk fees must disclose their true costs just like other payday loans. A tip is paid to a human being who serves you; it is not a legitimate way to disguise the cost of predatory loans.”

The proposal addresses evasions such as these:

- EarnIn disclosed 0% APR for a $100 loan but inserted a so-called tip of $11; with a $4 expedite fee included, the true APR would be 498%. California’s regulator found that 73% of transactions that solicited tips included them and identified “multiple strategies that lenders use to make tips almost as certain as required fees.”

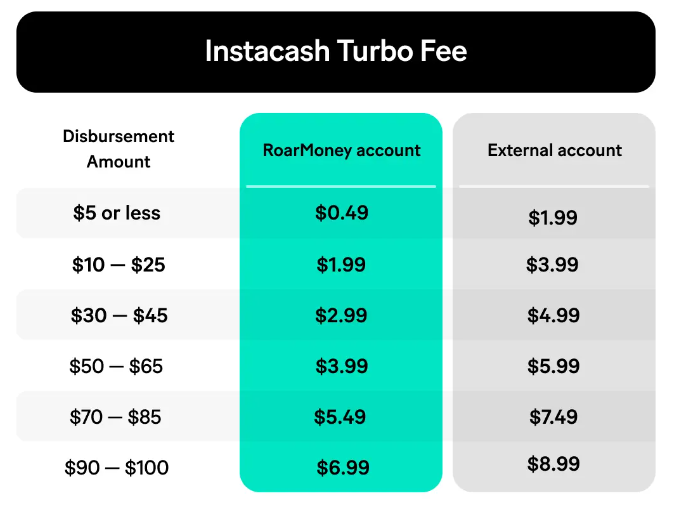

- The cost of sending loans instantly is 4.5 cents or lower, but MoneyLion charges an inflated “turbo fee,” which increases as the loan increases, up to $8.99 for an advance of $100, while claiming “no interest.”

{kind=link}

“Workers should not have to pay to be paid,” said Michael Best, senior attorney at the National Consumer Law Center. “Employers should pay a living wage and offer early pay for free as a benefit. They should not enable new forms of payday loans that extract fees from workers for borrowing from their next paycheck when the last one wasn’t enough.”

The CFPB released data from several lenders that offer paycheck advances through employers, finding that the average worker is stuck in a cycle of reborrowing, taking out 27 loans a year (and some over 40) with an average APR over 100%, but potentially as high as 580.4%. While some employers offer early pay for free, the CFPB found that over 90% of workers paid one or more fees, primarily expedite fees, and that speed was an “integral feature” of the credit.

California data on both employer-based and direct-to-consumer loans found average APRs for both types over 330% and an average of 36 loans a year. Other research shows that cash advance apps lead to an increase in overdraft fees, just like other payday loans.

Though the proposal only addresses federal law, it should send a message to states as well. “Fintech payday lenders have been pushing bills that say their loans are not loans and that authorize 300% APRs. It’s a page out of the playbook of payday lenders, who got established by claiming they were just offering ‘deferred presentment’ of post-dated checks,” Saunders said. “States that do not want to legalize a new form of fintech payday loan should listen to the CFPB and ignore the myth that earned wage or other cash advances are not loans.”

This year, 192 labor, consumer and civil rights groups opposed a bill that would have exempted earned wage advances from TILA. In 2021, 96 groups urged the CFPB to rescind the 2020 advisory opinion. The groups also urged the CFPB to rescind the related no-action letter given to PayActiv, which the CFPB did in 2022.

“The CFPB has made clear that earned wage advances are old wine in new bottles and that fintech lenders are not above the law,” Saunders added.

Related Resources

- CFPB’s SoLo Funds Enforcement Action is a Warning for Fintech Payday Lenders, May 20, 2024

- Consumers Need Strong Protections from Fintech Cash Advances that Create Debt Traps, Oct. 11, 2023

- State Recommendations for Earned Wage Advances and Other Fintech Cash Advances, Oct. 11, 2023

- Earned Wage Advances and Other Fintech Payday Loans: Workers Shouldn’t Pay to be Paid, April 20, 2023

- Data on Earned Wage Advances and Fintech Payday Loan “Tips” Show High Costs for Low-Wage Workers, April 10, 2023

- CFPB Urged to Reverse Earned Wage Actions that Threaten to Create Dangerous Fintech Payday Loan Loopholes, Oct. 12, 2021

Support NCLC

Please support NCLC's work to advance consumer rights and economic justice with a tax-deductible contribution today!

Donate