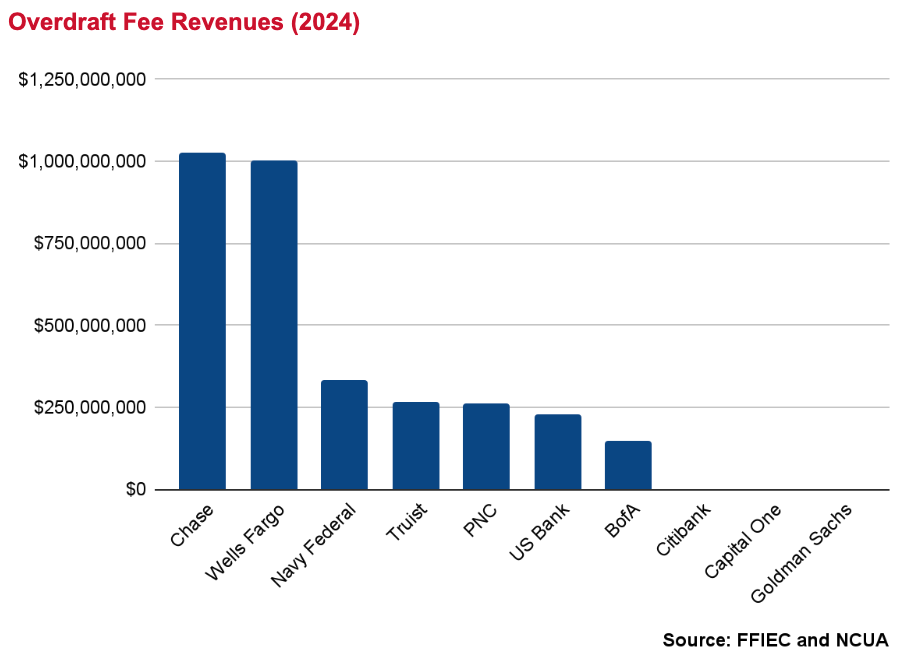

Overdraft fees can be a significant source of profit. Financial institutions differ in the tactics used to increase or decrease the fees paid by struggling families and the amount of fees they collect. Among the 10 largest banks, JPMorgan Chase and Wells Fargo stand out, with $1 billion in overdraft fees in 2024, nearly four times more than the next highest bank. The largest credit union, Navy Federal, which caters to the military community, collected $335 million, more than any of the biggest banks besides Chase and Wells Fargo despite its smaller size.

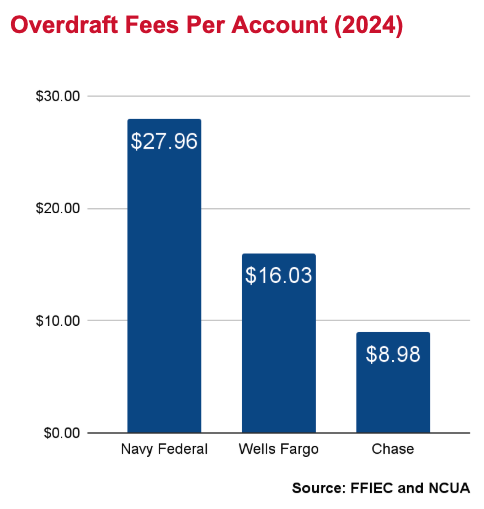

Adjusted for size, Navy Federal’s overdraft fees are especially glaring, showing the disproportionate impact that large fees have on Navy Federal’s military and civilian families. Navy Federal extracted nearly twice as much in overdraft fees per account as Wells Fargo and more than three times as much as Chase. Military families are also impacted by high fees at Wells Fargo and Chase, which offer military banking.

The Consumer Financial Protection Bureau’s (CFPB) overdraft fee rule would reduce back-end overdraft fees at very large financial institutions to $5 or the bank’s costs, whichever is greater. Institutions could offer overdraft lines of credit with no price limit, but they would be required to disclose the annual percentage rate (APR).

The rule will eliminate the incentive for banks and credit unions to push people into overdrafting or to use unfair practices to increase overdraft fees. Navy Fed, for example, was forced by the CFPB to pay $95 million for charging illegal surprise overdraft fees when customer accounts showed sufficient funds at the time of purchase. The rule is expected to save $225 per year for the average family that pays overdraft fees, and much more than that for the hardest hit families and those at institutions with especially abusive overdraft fee practices.

Methodology

Overdraft fee revenue in 2024 for the 10 largest banks by asset size, along with the largest credit union, was taken from call reports collected by the Federal Financial Institutions Examination Council (FFIEC) and the National Credit Union Administration (NCUA). While the FFIEC data includes nonsufficient funds (NSF) fees, all of the banks listed above have eliminated NSF fees. Citibank and Capital One show negligible remaining overdraft fees, but both banks have stopped charging the fees. Overdraft fee revenues reported for 2024 are:

| JPMorgan Chase Bank | $1,028,000,000 |

| Wells Fargo Bank | $1,000,000,000 |

| Navy Federal Credit Union | $335,071,586 |

| Truist Bank | $266,000,000 |

| PNC Bank | $260,979,000 |

| U.S. Bank | $229,797,000 |

| TD Bank | $229,560,000 |

| Bank of America | $148,000,000 |

| Citibank | $1,000,000 |

| Capital One | $170,000 |

| Goldman Sachs | $0 |

To obtain overdraft fees per account, for Chase and Wells Fargo, total overdraft fees were divided by the FFUEC call report line for the number of deposit accounts (excluding retirement accounts) of $250,000 or less. Navy Federal’s overdraft fees were divided by the NCUA call report line for total number of share draft accounts.

See all resources related to: Banking, Payments & Remittances